[ad_1]

nespix/iStock via Getty Images

Horizon Technology Finance Corporation (NASDAQ:HRZN) suffered a 24% valuation cut in 2022, and the business development company is now worth buying at book value.

Horizon Technology Finance is a high-yielding, technology-focused BDC with a yield that recently surpassed 10%. To support its growth, the business development company has a secured, debt-oriented investment portfolio.

Horizon Technology Finance’s credit portfolio is performing well, and the stock could eventually trade at a higher book value multiple.

Another Gem In the BDC Sector

Business development companies have suffered significant valuation losses in 2022, owing to investors’ expectation that recession factors will have an impact on the sector’s prospects for book value growth.

During recessions, it is more difficult for business development firms to produce positive growth in key metrics such as net investment income (due to portfolio income pressure) and book value (due to pressure on credit quality which tends to increase during recessions).

With that said, I believe it is time for dividend investors to target BDCs that, due to their credit performance and floating rate exposure, have the potential to outperform the sector.

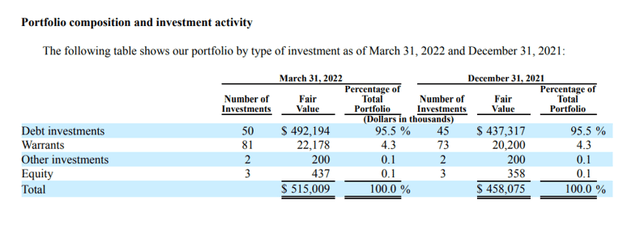

Horizon Technology Finance is a monthly-paying specialty finance company with a rapidly expanding investment portfolio. The portfolio had 50 debt investments and 81 warrant positions as of March 31, 2022.

Debt investments made by the BDC are typically Senior Term Loans that provide the BDC with a high level of capital protection. In March, the company’s debt, warrant, and equity positions were valued at $515 million, and the BDC was invested at a 12.4% annualized average portfolio yield.

Portfolio Composition (Horizon Technology Finance)

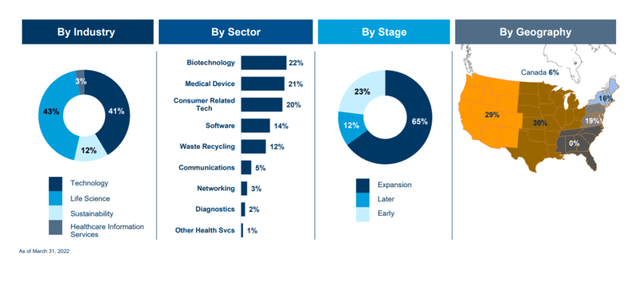

Horizon Technology Finance is an interesting dividend investment because it primarily invests in development-stage companies in the technology, life science, healthcare information, and services industries, and it participates in the upside of those companies through equity and warrant positions.

Horizon Technology Finance is similar in many ways to Hercules Capital, another BDC that seeks to capitalize on equity upside in specific technology niches.

Horizon Technology Finance has developed and nurtured a technology-focus in venture capital, which is where the BDC sees the greatest opportunity for high returns. The BDC is well-diversified and steers clear of cyclical industries that pose earnings and cash flow risks. Biotechnology as an industry accounts for 22% of the BDC’s total industry exposure.

Investments Overview (Horizon Technology Finance)

NII Exceeds Distributions

Horizon Technology Finance’s portfolio generated $1.41 per share in net investment income in 2021, while BDC paid out $1.25 per share, implying an 89% pay-out ratio. The dividend pay-out ratio was 90% from 2019 to 2021, so investors can reasonably assume that the $0.10 per share monthly dividend is sustainable.

Sail Through The Next Interest Rate Hiking Cycle With Horizon Technology Finance

The central bank is aggressively raising rates, making now an excellent time to select BDCs with the greatest amount of floating rate exposure.

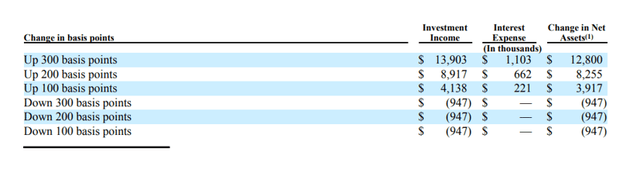

Horizon Technology Finance structures its finance deals carefully to ensure 100% floating rate exposure, which means HRZN has more floating rate exposure than the average business development company in the sector.

This means that a significant increase in interest rates will benefit Horizon Technology Finance more than other BDCs. Based on the BDC’s interest sensitivity table, a 200-basis-point increase in interest rates is expected to result in a $8.26 million increase in Horizon Technology Finance’s net assets.

Interest Sensitivity (Horizon Technology Finance)

Trading At Book Value

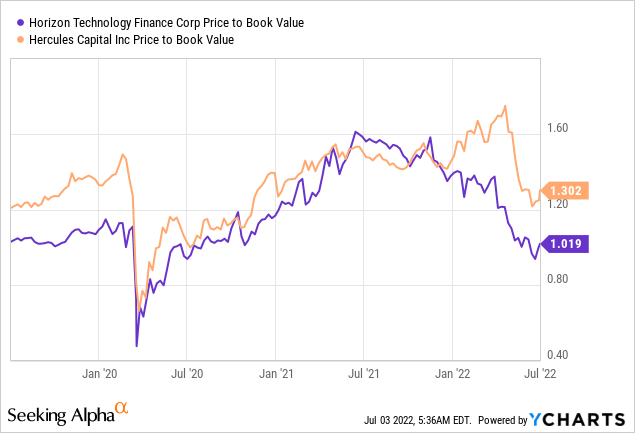

Because of their similarities in targeted industries and deal structures, I believe Hercules Capital is the best comparable for Horizon Technology Finance. Hercules Capital has a P/B ratio of 1.3x, owing to the BDC’s huge success with its tech-focused investment strategy that combines interest payments with equity upside.

Because the market rewards HTGC for the consistency of its portfolio results, the BDC trades at a premium to book value. Horizon Technology Finance currently has a P/B ratio of 1.0x, implying that HRZN may be a better buy than Hercules Capital based solely on book value.

Are There Any Asset Quality Problems?

Right now, I don’t see any major issues. Horizon Technology Finance had one loan that was past due as of March 31, 2022. The cost of this investment was $11.9 million, and the fair value was $5.5 million. On a fair value basis, the non-accrual ratio was about 1%, based on the total portfolio value of $515 million.

Why Horizon Technology Finance Could See A Lower Stock Price

To receive up-to-date information about Horizon Technology Finance’s portfolio performance, investors should closely monitor the BDC’s book value trend and non-accrual ratio. With only one non-accrual investment, I’d say portfolio quality is strong, but things can always change for the worse, especially if the BDC sector is destabilized by a recession.

My Conclusion

Now that Horizon Technology Finance is trading at book value, the proposition becomes more appealing.

HRZN is one of the best bets in the BDC sector for rising interest rates because it is 100% exposed to floating rates.

The dividend is covered and reasonably safe, while non-accruals are kept to a minimum.

Horizon Technology Finance is distinguished by its technological focus, and equity appreciation results in the payment of special dividends.

[ad_2]

Source link

More Stories

Marketing Strategies That Actually Drive Growth

Must-Know Business News to Stay Ahead in 2024

The Latest Business News Shaping the Global Market